FTC to Host Roundtable Discussion on October 4 on Artificial Intelligence and the Creative Fields

[ad_1]

Join the discussion on Twitter using the hashtag #GenAIchat.

[ad_2]

Source link

[ad_1]

Join the discussion on Twitter using the hashtag #GenAIchat.

[ad_2]

Source link

[ad_1]

New data from the Federal Trade Commission shows that scams originating on social media have accounted for $2.7 billion in reported losses since 2021, more than any other contact method.

In a new data spotlight, the FTC also takes a deep dive into social media scam trends in the first half of 2023. Reports during the first half of the year show that the most frequently reported scams on social media are related to online shopping, with 44 percent of reports pointing to fraud related to buying or selling products online. Most of these reports come from people who never received the items they ordered after responding to an ad on Facebook or Instagram.

While online shopping scams are the most commonly reported scam on social media, the spotlight notes that scams using social media to promote bogus investment schemes account for larger overall losses, accounting for 53 percent of all the money reported lost to scams on social media in the first half of the year. Cryptocurrency played a significant role in the investment scams consumers reported; more than half of the reports showed that consumers paid the scammers using cryptocurrency.

After investment scams, the spotlight noted that romance scams accounted for the second-most reported scam losses on social media.

The FTC recommends that consumers take steps to limit who can see their posts or contact them on social media, and to reach out directly by phone if someone claiming to be a friend or relative messages on social media asking for money. A full list of tips for consumers is included in the spotlight.

[ad_2]

Source link

FTC Data Shows Consumers Report Losing $2.7 Billion to Social Media Scams Since 2021 Read More »

[ad_1]

Two groups of student loan debt relief scammers will be permanently banned from the debt relief industry and are required to turn over their assets as part of a settlement with the Federal Trade Commission.

In the FTC’s May 2023 complaints against SL Finance LLC and its owners Michael Castillo and Christian Castillo, and BCO Consulting Services Inc. and SLA Consulting Services Inc. and their owners Gianni Olilang, Brandon Clores, Kishan Bhakta, and Allan Radam, the agency said that the defendants pretended to be affiliated with the U.S. Department of Education, charged illegal junk fees, and lured students with repayment programs and loan forgiveness that did not exist.

The SL Finance defendants also falsely claimed that their program was part of the CARES Act or a similar COVID-19 relief program, according to the complaint. The agency charged that these operations bilked students out of millions of dollars.

Under the proposed orders with SL Finance, its owners, and BCO Consulting and its owners, the defendants will be permanently banned from debt relief of any kind. They will also be banned from making any misrepresentations about financial products or services and from using false statements to collect consumers’ financial information. The SL Finance order also imposes a partially suspended monetary judgment of $5.8 million which is largely suspended based on defendants’ inability to pay. The Castillo brothers will be required to surrender assets worth approximately $312,685. The BCO Consulting orders imposes a partially suspended monetary judgment of $5.8 million, which is also largely suspended based on the defendants’ inability to pay. Individual defendants Olilang, Clores, Bhakta, and Radam will be required to relinquish assets worth approximately $565,594.

If any of the defendants are found to have materially misrepresented their finances, the full amount of the monetary judgment would become immediately due from that defendant.

The Commission votes approving the stipulated final orders were 3-0. The FTC filed the proposed orders in the U.S. District Court for the Central District of California.

NOTE: Stipulated final orders have the force of law when approved and signed by the District Court judge.

The lead staff attorneys on this matter are Katherine Aizpuru and Samuel Jacobson of the FTC’s Bureau of Consumer Protection.

[ad_2]

Source link

[ad_1]

As a result of a Federal Trade Commission lawsuit, the owner of a series of companies that charged consumers millions of dollars in undisclosed and recurring subscription fees for skin creams has agreed to a lifetime ban on negative option marketing and will turn over his funds and assets to the FTC.

The FTC sued Gopalkrishna Pai and eight companies he owned in 2019, charging that he marketed a number of skin creams online, selling them for a nominal “shipping and handling” fee, usually $4.99. Consumers who bought the products were not aware that they would later be charged the full price for the products and a recurring monthly charge.

“Our proposed order banning defendants from the subscription marketing business and ordering the return of assets is a big win for consumers, and it should send a strong message to other unscrupulous marketers,” said Samuel Levine, Director of the FTC’s Bureau of Consumer Protection. “The FTC will continue its crackdown on junk fees and subscription traps.”

In its complaint, the FTC alleged that Pai and his companies charged consumers tens of millions of dollars in fees they didn’t consent to, noting that the supposed disclosure of these fees was hidden behind a small link on the sales websites, and that consumers’ attempts to cancel were often unsuccessful, even when they returned the products unopened. The FTC also alleged that Pai created hundreds of shell companies to facilitate payment processing for the scam.

In 2022, Pai pled guilty to separate charges brought by the U.S. Attorney’s Office for the District of Puerto Rico related to his actions.

The proposed settlement order in the FTC case, includes a number of requirements:

The order contains a total monetary judgment of $34,081,6073, which is partially suspended based on the settling defendants’ inability to pay the full amount. If the settling defendants are found to have lied to the FTC about their financial status, the full judgment would be immediately payable.

The Commission vote approving the stipulated final order was 3-0. The FTC filed the proposed order in the U.S. District Court for the District of Puerto Rico.

NOTE: Stipulated final orders or injunctions have the force of law when approved and signed by the District Court judge.

The lead staff attorney on this matter was Michelle Schaefer of the FTC’s Bureau of Consumer Protection.

[ad_2]

Source link

[ad_1]

The Federal Trade Commission today announced a new proposed rule to prohibit junk fees, which are hidden and bogus fees that can harm consumers and undercut honest businesses. The FTC has estimated that these fees can cost consumers tens of billions of dollars per year in unexpected costs.

The agency launched a proceeding last year requesting public input on whether a rule would help to eliminate these unfair and deceptive charges. After receiving more than 12,000 comments on how fees affect their personal spending or business, the FTC is seeking a new round of comments on a proposed junk fee rule.

“All too often, Americans are plagued with unexpected and unnecessary fees they can’t escape. These junk fees now cost Americans tens of billions of dollars per year—money that corporations are extracting from working families just because they can,” said FTC Chair Lina M. Khan. “By hiding the total price, these junk fees make it harder for consumers to shop for the best product or service and punish businesses who are honest upfront. The FTC’s proposed rule to ban junk fees will save people money and time, and make our markets more fair and competitive.”

As the public comments made clear, consumers are fed up with hidden fees for everything from booking hotels and resort fees to buying concert tickets online, renting an apartment, and paying utility bills. Many consumers said that sellers often do not advertise the total amount they will have to pay, and disclose fees only after they are well into completing the transaction. They also said that sellers often misrepresent or do not adequately disclose the nature or purpose of certain fees, leaving consumers wondering what they are paying for or if they are getting anything at all for the fee charged.

The proposed rule will save consumers more than 50 million hours per year of wasted time spent searching for the total price in live-ticketing and short-term lodging alone, according to FTC estimates. This time savings is equivalent to more than $10 billion over the next decade.

The Proposed Rule

The proposed rule would ban businesses from running up the bills with hidden and bogus fees, ensure consumers know exactly how much they are paying and what they are getting, and help spur companies to compete on offering the lowest price. Businesses would have to include all mandatory fees when telling consumers a price, making it easier for consumers to comparison shop for the lowest price. The proposed rule would also have enforcement teeth, allowing the FTC to secure refunds for harmed consumers and seek monetary penalties against companies that do not comply with its provisions.

To accomplish this, the proposed rule would ban the following junk fee practices that consistently confuse and trick consumers:

These provisions are aimed at ensuring businesses will no longer be able to lure consumers with artificially low prices that they later inflate with mandatory fees or to deceive consumers about the nature and purpose of fees. In addition, the proposed rule would provide a level playing field for honest businesses by requiring all businesses to quote total prices at the start of the purchasing process and to remove false or misleading information about fees from the marketplace.

Other Federal Agencies’ Actions

Other federal agencies and organizations are joining the FTC to develop and implement rules prohibiting junk fees across multiple U.S. markets and sectors including the Consumer Financial Protection Bureau (CFPB), the Federal Communications Commission (FCC), the Department of Housing and Urban Development (HUD), and the Department of Transportation (DOT).

“Americans are fed up with the junk fees that are creeping across the economy,” said CFPB Director Rohit Chopra. “The FTC’s proposed rule will protect families and honest businesses from race-to-the-bottom abuses that cost us billions of dollars each year. If finalized, the CFPB will enforce the rule against violators in the financial industry and ensure that these firms play fairly.”

“No one likes surprise charges on their bill. Consumers deserve to know exactly what they are paying for when they sign up for communications services. But when it comes to these bills, what you see isn’t always what you get,” said FCC Chairwoman Jessica Rosenworcel. “Instead, consumers have often been saddled with additional junk fees that may exorbitantly raise the price of their previously agreed-to monthly charges. To combat this, we’re implementing Broadband Consumer Labels, a new tool that will increase price transparency and reduce cost confusion, help consumers compare services, and provide ‘all-in-pricing’ so that every American can understand upfront and without any surprises how much they can expect to be paying for these services.”

“I believe that every renter should know the true cost of finding and staying in their home and not be hit with hidden costs and junk fees. Earlier this year, we called for reform in the housing industry to increase transparency for renters across the country, reflecting the Biden-Harris administration and the Department of Housing and Urban Development’s commitment,” said HUD Secretary Marcia L. Fudge. “HUD continues to release research and data highlighting state, local, and private sector policies to encourage fairness and equity in the rental market.”

“Junk fees mean that working families have to pay higher prices for the things they need, which is why President Biden is taking decisive action to eliminate them,” said U.S. Transportation Secretary Pete Buttigieg. “At DOT, we have secured commitments from major U.S. airlines to provide free rebooking, meals, and hotels when they are responsible for stranding passengers. We’re working to stop airlines from forcing parents to pay to sit next to their kids, and requiring them to disclose hidden fees for things like extra bags. And we’ve helped secure billions of dollars in refunds for passengers whose flights are cancelled.”

The Commission vote approving publication of the notice of proposed rulemaking was 3-0. Once the notice has been published in the Federal Register, consumers can submit comments electronically for 60 days. Consumers also may submit comments in writing by following the instructions in the “Supplementary Information” section of the Federal Register notice.

[ad_2]

Source link

FTC Proposes Rule to Ban Junk Fees Read More »

[ad_1]

The Federal Trade Commission and the Consumer Financial Protection Bureau (CFPB) obtained a settlement that will require credit reporting agency Trans Union LLC and a subsidiary to pay a total of $15 million to settle charges they failed to ensure the accuracy of tenant screening reports by including inaccurate and incomplete eviction records about consumers, hampering their ability to obtain housing.

In a complaint filed in federal court, the FTC and CFPB say that Colorado-based TransUnion Rental Screening Solutions, Inc. (TURSS) and its parent company, Trans Union LLC, based in Chicago and commonly known as TransUnion, violated the Fair Credit Reporting Act (FCRA) by failing to ensure the accuracy of the information included in their tenant background screening reports.

“Consumers struggling to find housing shouldn’t be shut out by tenant screening reports that are ridden with errors and based on data from secret sources,” said Samuel Levine, Director of the FTC’s Bureau of Consumer Protection. “Protecting consumers looking for housing is critical to a fair economy, and we are proud to partner with the CFPB in obtaining this record-breaking order.”

“Americans across the country were put at risk of wrongful housing denials because TransUnion failed to follow the law,” said CFPB Director Rohit Chopra. “We are ordering TransUnion to cease its yearslong illegal activity, clean up its broken business practices, redress its victims, and pay penalties.”

TURSS provides background screening reports about consumers to thousands of clients, including rental property owners, property management companies, employers, and other background screening companies, for tenant and employee selection. These reports may include information about consumers’ criminal and eviction records, including the amount sought by a landlord in court, any judgment amount the court may award, and the amounts owed by consumers. Trans Union LLC manages and oversees TURSS’s compliance with the FCRA.

Inaccurate and outdated information in tenant screening reports can significantly hamper consumers’ ability to find housing, costing them time and money by prolonging their search for housing, requiring them to pay additional application fees and spend time correcting errors in their background reports.

TURSS obtains eviction records from third-party provider LexisNexis Risk and Information Analytics Group, Inc. but has failed to take steps to ensure the accuracy of the data it was provided, according to the complaint. The FTC and CFPB say TURSS failed to follow reasonable procedures to: prevent the inclusion of multiple entries for the same eviction case; accurately report the disposition of eviction cases it included in its reports; accurately label the monetary amounts associated with those cases; and prevent the inclusion of sealed eviction records in its background reports.

Until April 2021, TURSS often reported developments in the same eviction proceeding as separate events, making it appear as if a consumer had more than one eviction, according to the complaint. The company took steps to change that practice only after learning of the FTC’s investigation. The company also failed to follow reasonable procedures to accurately report the outcome of evictions, such as reporting an eviction was filed without reporting that it was also dismissed months or years before, or reporting that a landlord was awarded a judgment in an eviction proceeding when the case was actually dismissed.

The company also included inaccurate labels in its reports that mischaracterized the nature of certain information in consumers’ eviction records, according to the complaint. The company labeled money that a landlord claimed a consumer owed as “Judgment Amount,” giving the false impression that this was the amount awarded by a court. The complaint also charges that TURSS failed to put in place reasonable procedures to prevent eviction records that had been sealed, or restricted from public view, by a court from appearing in its reports.

The FTC and CFPB also say that TURSS violated the FCRA by failing in many instances to provide consumers with the names of third-party vendors from whom it received criminal and eviction records included in its tenant screening reports, which made it harder for consumers to correct errors in their background reports.

Under the proposed order, which must be approved by a federal court before it can go into effect, TURSS and Trans Union LLC will be required to pay $11 million, which will be used to compensate consumers, and a $4 million civil penalty, which will go to the CFPB’s civil penalty fund. This is the largest amount ever recovered in an FTC tenant screening matter. In addition, the companies must also take steps to address the allegations of the complaint and help enable consumers to dispute inaccurate information in the future, including:

The Commission vote authorizing the staff to file the complaint and stipulated final order was 3-0. The FTC and CFPB filed the complaint and stipulated final order in the U.S. District Court for the District of Colorado.

NOTE: The Commission files a complaint when it has “reason to believe” that the named defendants are violating or are about to violate the law and it appears to the Commission that a proceeding is in the public interest. Stipulated final orders have the force of law when approved and signed by the District Court judge.

The lead staffers on this matter are Jarad Brown and Whitney Moore in the FTC’s Bureau of Consumer Protection.

[ad_2]

Source link

[ad_1]

The Federal Trade Commission announced a settlement with bankrupt crypto company Voyager that will permanently ban it from handling consumers’ assets and is filing suit against its former CEO, Stephen Ehrlich, for falsely claiming that customers’ accounts were insured by the Federal Deposit Insurance Corporation (FDIC) and were “safe,” even as the company was approaching an eventual bankruptcy. The complaint also names Stephen Ehrlich’s wife, Francine Ehrlich, as a relief defendant.

In the federal court complaint, the FTC charges that from at least 2018 until it declared bankruptcy in July 2022, Voyager used promises that consumers’ deposits would be “safe” to entice them to hand over their funds. When the company failed, consumers lost access to significant assets they had saved, including ongoing salary deposits, college tuition funds, and down payments for homes, according to the complaint, which notes that consumers were locked out of their cash accounts for more than a month and lost more than $1 billion in crypto assets.

“Consumers reported over $1.4 billion in losses to cryptocurrency scams in the last year, and the FTC continues to crack down on those who lie to consumers about these risky assets,” said Samuel Levine, Director of the FTC’s Bureau of Consumer Protection. “This action reminds companies and individuals: don’t play fast and loose with claims about FDIC insurance.”

The proposed settlement with Voyager and its affiliates will permanently ban the companies from offering, marketing, or promoting any product or service that could be used to deposit, exchange, invest, or withdraw any assets. The companies also agreed to a judgment of $1.65 billion, which will be suspended to permit Voyager to return its remaining assets to consumers in the bankruptcy proceedings. Former executive Stephen Ehrlich has not agreed to a settlement and the FTC’s case against him will proceed in federal court.

According to the complaint, Voyager enticed consumers to deposit cash and cryptocurrency with the company based on assurances that their assets were especially safe on the platform. The company offered incentives to consumers who converted the cash they deposited into a cryptocurrency called USD Coin, a so-called “stablecoin” that claims to track the value of the U.S. dollar.

The company’s marketing included direct promises about the safety of consumers’ deposits. One example cited in the complaint included the line “YOUR USD IS FDIC INSURED”

Voyager, however, is not a bank or financial institution, and the deposits consumers made with Voyager were not eligible to be insured by the FDIC. The complaint notes that the FDIC does not insure crypto assets at all, and consumers’ cash deposits were actually placed in an account held by Voyager at a traditional bank that also issued debit cards on behalf of Voyager. Consumers’ cash was only protected if that bank itself failed, and their cryptocurrency wasn’t protected at all.

The complaint notes that Voyager was aware that the company’s claims could mislead consumers. The bank where Voyager deposited consumers’ funds contacted the company in 2021 saying the claims were “potentially misleading.” A bank representative went on to say that “a reasonable consumer could conclude that his USDC [USD Coin] held with Voyager is FDIC-insured.” While Voyager made some changes to its cardholder agreement, the complaint notes that the company continued its misleading advertisements. The company only removed the FDIC claims from its advertising after receiving a cease-and-desist letter from the FDIC.

Ehrlich himself, in a June 2022 letter to Voyager customers, reassured them of the company’s stability, claimed it was “well-capitalized and positioned to weather the bear market,” and said that consumers’ funds were “as safe with us as at a bank.”

Two weeks later, the company froze consumers’ access to their accounts.

The FTC staff complaint alleges that Voyager and Stephen Ehrlich violated the FTC Act’s prohibition on deceptive practices and the Gramm-Leach-Bliley Act’s prohibition on obtaining a customer’s financial information through false, fictitious, or fraudulent statements. The complaint also alleges that Stephen Ehrlich transferred millions of dollars to his wife Francine, including funds that can be traced directly to the alleged unlawful conduct.

In addition to banning Voyager and its affiliated companies from handling consumers’ assets, the proposed settlement prohibits the companies from misrepresenting the benefits of any product or service; from making false, fictitious, or fraudulent representations to any customer of a financial institution in order to obtain or attempt to obtain their financial information; and from disclosing nonpublic personal information about consumers without their express consent.

The Commission voted 3-0 to file a complaint against Voyager and its affiliated companies, Stephen Ehrlich, and relief defendant Francine Ehrlich and to approve a stipulated order with Voyager and its affiliated companies. The complaint was filed in the U.S. District Court for the Southern District of New York.

In a parallel action, on October 12, the Commodity Futures Trading Commission separately charged Ehrlich with fraud and registration failures.

NOTE: The Commission authorizes the filing of a complaint when it has “reason to believe” that the law has been or is being violated, and it appears to the Commission that a proceeding is in the public interest. Stipulated orders have the force of law when approved and signed by the District Court judge.

The staff attorneys on this matter are Quinn Martin, Sanya Shahrasbi, and Larkin Turner of the FTC’s Bureau of Consumer Protection.

[ad_2]

Source link

[ad_1]

A federal judge in Illinois has ruled in favor of the Federal Trade Commission in a case the FTC has been litigating since 2019 against a telemarketing company and its owners, finding they made millions of illegal, unsolicited calls to consumers on the Do Not Call Registry.

The court found that corporate defendants Day Pacer, LLC and Edutrek, L.L.C. purchased consumers’ contact information primarily from websites claiming to help people find jobs, and instead illegally called those consumers to market unsolicited vocational or post-secondary education services. The court also found that the defendants assisted and facilitated other telemarketing companies by paying them to make approximately 40 million calls to consumers on the Do Not Call Registry. Additionally, the court found that individual defendants Raymond Fitzgerald, Ian Fitzgerald, and David Cumming directly participated in or had authority to control the corporations’ deceptive acts or practices, and were therefore also liable.

The court found that the defendants knowingly violated the Telemarketing Sales Rule, citing evidence that the defendants had ignored repeated complaints from consumers and warnings from business partners.

In granting summary judgment, the court found that the FTC was entitled to both injunctive relief and civil penalties. The court has scheduled a hearing to determine the amount of the civil penalty award and the scope of injunctive relief.

[ad_2]

Source link

[ad_1]

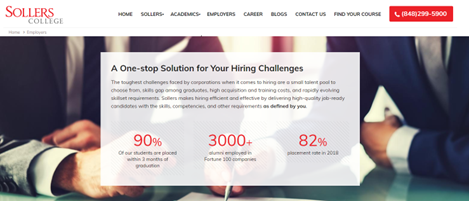

Sollers College and its parent company, Sollers Inc., have been ordered to cancel $3.4 million in student debt to resolve separate charges brought by the Federal Trade Commission and the state of New Jersey that said the companies lured prospective students to enroll by falsely touting their job-placement rates and that their relationships with prominent companies would lead to jobs after students graduate.

The for-profit school also had an illegal twist to the “income share agreements” it encouraged students to take out to pay for the school, according to the FTC’s complaint. Income-share agreements require students to pay the school a percentage of their future income in exchange for covering their tuition.

“Not only did Sollers College use deceptive advertisements to attract students, it trapped them in multi-year income share agreements that broke the law by leaving out important borrower rights,” said Samuel Levine, Director of the FTC’s Bureau of Consumer Protection. “Today’s order cancels all income-share agreements issued by the school. Companies that skirt long‑standing consumer protection laws when offering new financing products should be on notice that the FTC takes these violations seriously.”

According to the FTC’s complaint, Sollers, and its parent company, used their website, social media, and email campaigns to falsely advertise their partnerships with prominent employers in the fields of information technology, clinical research, and drug safety. Sollers falsely claimed that its partnerships with prominent employers, such as Pfizer, Weill Cornell Medicine, and Infosys, resulted in jobs for its graduates at those companies. In reality, many of the businesses featured on Sollers’ website had no partnership with the school at all.

According to the FTC’s complaint, Sollers, and its parent company, used their website, social media, and email campaigns to falsely advertise their partnerships with prominent employers in the fields of information technology, clinical research, and drug safety. Sollers falsely claimed that its partnerships with prominent employers, such as Pfizer, Weill Cornell Medicine, and Infosys, resulted in jobs for its graduates at those companies. In reality, many of the businesses featured on Sollers’ website had no partnership with the school at all.

The complaint states that, since at least 2018, Sollers advertised that the vast majority of Sollers graduates are placed in jobs. For example, the company advertised, “90% of our students are placed within 3 months of graduation,” on its website. In reality, the job placement rate for Sollers graduates is substantially lower than the 80 percent, 82 percent, 90 percent or “near perfect” rates featured prominently on its website and in its advertising campaigns. For example, the school’s own data suggests that the current job-placement rate for graduates of its Life Sciences programs remains as low as 52 percent.

In addition, the complaint notes that Sollers encouraged students to pay for their education using income-share agreements. Under the specific terms of Sollers’s contracts, students agreed to pay Sollers a fixed percentage of their future income on a monthly basis, typically for two years. Between August 2018 and April 2021, the school entered into 392 illegal agreements, none of which included certain disclosures mandated by law. Specifically, the agreements failed to include the Holder Rule notice, which protects consumers who enter certain loans or credit contracts by preserving their right to assert claims and defenses, even if the loans or contracts are assigned to a third party. Sollers later sold a portion of the agreements to third parties.

Under the stipulated order, the for-profit is prohibited from falsely advertising any educational product or service. The order also prohibits the company from denying access to diplomas or transcripts based on any debt forgiven by the proposed order.

Specifically, Sollers must:

The Commission vote authorizing the staff to file the complaint and stipulated final order was 3-0. The complaint and stipulated final order will be filed in the U.S. District Court for the District of New Jersey.

The staff attorneys on this matter are Wendy Miller and Paul Mezan of the FTC’s Bureau of Consumer Protection.

NOTE: The Commission files a complaint when it has “reason to believe” that the named defendants are violating or are about to violate the law and it appears to the Commission that a proceeding is in the public interest. Stipulated final orders have the force of law when approved and signed by the District Court judge.

[ad_2]

Source link

[ad_1]

The Federal Trade Commission has issued its latest report to Congress on protecting older adults, which highlights key trends based on fraud reports by older adults, and the FTC’s multi-pronged efforts to combat the problem through law enforcement actions, rulemaking, and outreach and education programs.

In addition, the report calls on Congress to update the FTC Act in response to the Supreme Court’s 2021 ruling in the AMG Capital Management case, which severely limited the FTC’s ability to recover money that older adults and other consumers lose to scammers.

“We do all we can to protect older adults and shut down the scams targeting them,” said Samuel Levine, Director of the FTC’s Bureau of Consumer Protection. “But we still need Congress to restore our authority to get money back from the scammers and into consumers’ pockets.”

The report, Protecting Older Consumers, 2022-2023, A Report of the Federal Trade Commission, finds that older adults reported losing more than $1.6 billion to fraud in 2022.

Because the vast majority of frauds are not reported, this figure represents only a fraction of the overall cost of fraud to older consumers, which the FTC estimates to be as high as $48 billion. The report also finds that in 2022, older adults reported significantly higher losses to investment scams, business impersonation scams and government impersonation scams than they did in 2021:

As in prior years, the analysis of fraud reports received by the FTC in 2022 showed that adults aged 60 and over were substantially less likely to report losing money to fraud than adults aged 18-59. When they did report losing money, though, they tended to report losing substantially more than younger adults. Consumers 80 and older reported losing a median of $1,750 to fraud, while those in their seventies reported a median loss of $1,000, with both numbers increasing over 2021.

The analysis included in the report to Congress also found that adults 60 and older were more than six times as likely as adults aged 18 to 59 to report losing money to a tech support scam. Older adults were more than twice as likely to report a loss to a prize, lottery or sweepstakes scam, and 73 percent more likely to report losing money to a friend or family impersonation scam.

The report’s analysis shows that older adults filed the largest number of reports about online frauds—where consumers were first exposed to the fraud via social media, the web, or online ads. The largest median losses, however, were reported by older adults on fraud that started with a phone call. The impact of scams where older adults were contacted on social media also increased; the median reported loss from this type of scam jumped from $460 in 2021 to $800 in 2022.

The report focuses on key actions the FTC has taken to protect older consumers, particularly in light of the Supreme Court’s AMG Capital decision. In 2022, the Commission issued a notice of proposed rulemaking on government and business impersonation, which is aimed at curbing a form of fraud that has resulted in tremendous losses for older consumers. A new rule would offer additional tools for the FTC to seek refunds for consumers harmed by these scams.

In addition, the report notes a number of enforcement actions that had a particular impact on older consumers, including cases against Publishers Clearing House for using dark patterns to mislead consumers into thinking that making a purchase would increase their chances of winning the company’s sweepstakes drawing; a company that placed more than a billion calls to consumers, including hundreds of robocalls and calls to consumers on the National Do-Not-Call Registry; a bogus credit card relief scheme; a timeshare exit scam; a company making false health claims about COVID prevention; and current and former major distributors for the multi-level marketing company doTERRA for making baseless claims about COVID treatments. The report highlights a number of ongoing law enforcement partnerships in which the FTC works with other federal agencies, along with state and local authorities, to take actions to protect older consumers.

Finally, the report details the FTC’s outreach and education efforts through such programs as the Pass it On campaign, which focuses on providing fraud prevention resources to older adults so they can help protect their communities by sharing the information and materials with family and friends. It also details the FTC’s ongoing efforts to implement the Stop Senior Scams Act of 2022.

The Commission vote authorizing the report to Congress was 3-0.

[ad_2]

Source link

FTC Issues Annual Report to Congress on Agency’s Actions to Protect Older Adults Read More »